Executive Director’s Message: State Lowered TRS Funding by $500 Million

A lot of people throughout Illinois breathed a sigh of relief this summer.

The partisan political dispute that has consumed Springfield for three years broke just long enough in July to enact a state budget – the first since 2015. Illinois is still a long way from fiscal stability, but any small step forward is considered a good thing.

Well, what was good for almost everyone else in Illinois was, unfortunately, bad for TRS. Recognizing the pain felt across Illinois when there was no budget, it seems incredibly insensitive for me to say that TRS was better off without a budget.

How can that be?

During the budget impasse, contributions from state government to TRS and the other public pension systems were officially deemed a “priority payment” and ranked above most of the state’s other expenditures in part because the state’s credit rating hinged on whether Illinois was paying off its huge pension liabilities. The contribution amount was set by the existing funding formula found in state law. But when the fiscal year 2018 budget was enacted, the state’s contribution to TRS immediately dropped by $500 million. The new budget included changes to the formula that lowered the state’s obligation.

State government got a budget. TRS got less money.

Despite this reduction in fiscal year 2018 state support, TRS has – and will have – more than enough money to pay benefits for the foreseeable future. We currently have about $50 billion in the bank. Total investment income last year was $5.5 billion. Annually, our benefit payments total about $6 billion.

Still, the $500 million reduction in the state’s contribution is important for the long-term future of TRS. Our latest actuarial report shows TRS is 40 percent funded. An analysis presented to the TRS Board earlier this year demonstrated that the ability of TRS to remain solvent and pay benefits in the long-term is dependent on the state making its required statutory contributions.

But, as you may know, the state’s total pension contribution is roughly 25 percent of the total budget. That’s about four times higher than the typical burden for pensions paid by taxpayers in other states. Looking ahead, the state’s annual contribution is projected to grow by 3 percent annually. State revenues don’t grow that fast, so the pension burden only increases.

Reducing TRS’s appropriation this year, or in any year, clearly helps balance that year’s state budget. But it also means taxpayers who are not even born yet will be paying for this latest decision to kick the pension can down the road.

For every dollar reduced today, you need $3 in future contributions to make up for the investment income you won’t be able to generate because you didn’t have that dollar to invest. The $500 million reduction in fiscal year 2018 means that over the next 30 years, taxpayers will have to pay an additional $1.5 billion in state contributions to TRS.

But that’s not all. There’s another aspect of the new state budget that affects TRS – the creation of the “Tier 3” benefit structure for future teachers. Tier 3 was touted as a new solution to Illinois pension challenges. If only that were true.

The main challenge facing TRS is the unfunded liability carried by the System since 1939. That liability, currently $73 billion, is exclusively a Tier 1 problem created by decades of state government underfunding. In response, state officials have enacted two major overhauls of the Illinois Pension Code since 2010 – Tier 2 and now, Tier 3.

Tier 2 helps a little. Tier 2 members pay for their entire benefit through their payroll contributions, which means the state will not have to contribute anything to pay these benefits. At the same time, Tier 2 members subsidize Tier 1 members. Tier 2 members pay 9 percent for a benefit that only costs 7 percent. That overpayment will create a subsidy of $10 billion to $15 billion over time.

Tier 3 will not help at all. Tier 3 members also will pay for their entire retirement benefit. But there will be no subsidy for Tier 1 from Tier 3. All it does is create a third set of benefits. With that said, TRS is required by law to implement Tier 3 “as soon as possible.”

We’ve done a lot in recent months to prepare the groundwork for Tier 3. The first step requires a major shift in the way TRS does business. Right now school districts report information on member salaries, contributions and service time annually. Tier 3 will require monthly reports.

We have met with officials from public pension systems in Illinois and other states that have converted to monthly reporting. We want to learn what they did right and what to avoid as we move forward. We have started mapping out the information technology and procedural changes that will be required.

Our goal is to present a preliminary time line for the implementation of Tier 3 to the TRS Board in March of 2018. As I have said previously, we anticipate that the earliest date for Tier 3 is July 1, 2019. Right now, we’re aiming at that goal.

Best Wishes,

Dick Ingram

Even with Good Investment Returns, Financial Future Remains “Guarded”

Despite very good investment returns in fiscal year 2017 and over the last 30 years, the long-term fiscal outlook for TRS remains guarded, at best, due to a heavy unfunded liability and decades of inadequate government contributions.

TRS investments generated a positive 12.6 percent rate of return, net of fees, during fiscal year 2017 – a return that exceeded the System’s custom investment benchmark of 11.4 percent. TRS ended fiscal year 2017 with $49.4 billion in assets. Total investment income was $5.5 billion. The 30-year investment return for TRS was 8.1 percent, net of fees, which exceeds the System’s current long-term investment goal of 7 percent.

“Our investments performed well during fiscal year 2017 and that’s always good news,” said TRS Executive Director Dick Ingram. “Even better is the fact that our portfolio is structured to deliver these returns while taking on less investment risk than most of our peers. Risk management is critical because we know we can’t invest our way out of our funding shortfall. The TRS unfunded liability was created by seven decades of inadequate funding by state government and our future sustainability relies on consistent state funding to pay down this debt.”

Even with these long-term concerns, TRS has more than enough money on hand to pay member benefits for the foreseeable future.

Ingram stressed that the 30-year rate of return of 8.1 percent is the most important number in the fiscal year 2017 investment data. The 30-year time frame not only reflects the long-term relationship that TRS has with its members but indicates a successful investment program over several generations.

While the funded status improved modestly during fiscal year 2017 from 39.8 percent to 40.2 percent, at the same time the System’s unfunded liability increased. The TRS unfunded liability was $73.4 billion at the end of the fiscal year, compared to $71.4 billion at the end of fiscal year 2016.

Since its founding in 1939, the state has never appropriated an annual contribution to TRS that actuaries say has equaled annual “full funding.”

In December, the TRS Board of Trustees approved a $4.47 billion state contribution to TRS for fiscal year 2019, a 9.02 percent increase over the current year’s contribution of $4.10 billion. Both the fiscal year 2019 and 2018 contributions fall $2.9 billion below the full funding threshold.

The TRS unfunded liability is one of the largest burdens faced by any public pension plan in the nation, and that liability threatens the long-term financial stability of the System because each year more and more revenue must be dedicated to paying off a debt that began accumulating in 1939. During fiscal year 2017, 80 percent of state government’s $3.98 billion contribution, or $3.2 billion, was dedicated to the unfunded liability. The cost of teacher pensions was approximately $800 million.

“State government continues its historic underfunding of TRS and the result, year after year, is a higher unfunded liability for TRS and more uncertainty for our members,” Ingram said. “The financial hole TRS faces keeps getting deeper. TRS investments are performing well over the long haul, but it’s not enough to make up for almost 80 years of under-sized state contributions.”

TRS Benefits Report Available Online for Active and Inactive Members

In late November, active and inactive members were emailed that their 2017 TRS Benefits Reports were available online.

Reports are only sent to members who are not yet collecting a benefit. Retirees do not receive TRS Benefits Reports. The report summarizes the following information about a member’s TRS account: service credit, refundable contributions, beneficiary refund, beneficiaries, sick leave service, and 2.2 upgrade information.

If you are an active or inactive member who has not provided your email address to TRS and you received this newsletter by mail, please visit https://www.trsil.org. Then, set up an account under “Member Login” on the home page. You will need your member ID. If you do not know it, call us at 877-927-5877 (877-9-ASK-TRS). You will be able to view your TRS Benefits Report after signing in. Additionally, please enter your email address under the contact information in the secure area so you will receive future emails from us.

Recent payments and changes in outstanding balances will not be reflected on your report, but will be shown in your online account. If you need to change your beneficiaries, complete a Member Information and Beneficiary Designation (MIBD) form: https://www.trsil.org/MIBD_form. Please print out and mail the form to us and we will update your file. A new MIBD form replaces any former version on file with TRS. If you see an error on your reported service record or salaries, contact your employer (school district) without delay to correct the problem. This information is reported by your employer on your behalf to TRS. It may be more difficult to correct an error if you wait until retirement.

Please call us if you believe your report has an error (other than salary or service credit), if you need an additional copy or if you have any questions about the content.

Post-Retirement Employment Limitations Apply to All Retirees

In recent months, TRS has become aware that in an effort to overcome a shortage of classroom teachers in Illinois, some TRS-covered districts are contracting with private companies to provide them with licensed, experienced staff to fill classroom positions. Often, these contract teachers are retired educators receiving a TRS pension benefit.

All retired TRS members who return to teaching must follow the post-retirement employment limitations set by state law, even if they are employed by a private company that contracts with a school district to provide teachers.

It is the responsibility of all retired teachers to observe all post-retirement limitations. TRS will suspend a retired teacher’s benefit if the teacher exceeds the limitations regardless of whether he/she is employed by a school district or a private corporation.

A brief primer follows on the post-retirement work limitations set in state law:

- Following your retirement, you may not resume employment in a TRS-covered position, including substitute and summer school teaching, in the same school year in which you last contributed to TRS. The official school year is July 1 through June 30. If you retire during the school year, you may teach summer school only if the first day of that teaching service is after June 30.

- In the school year following the school year in which you last contributed to TRS, you may be employed in a TRS-covered position for up to 100 paid days or 500 paid hours per school year and still receive your TRS annuity/benefit. Only work that requires teacher licensure is subject to these limitations.

- If you resume TRS-covered employment in the same school year that you last contributed to TRS as an active member, you must repay all annuity payments received from the day of retirement. All annuity payments must be repaid if you exceed the limits during your first school year in retirement.

- For post-retirement employment purposes, the Illinois Pension Code says one full day of service is equal to five hours. Read https://www.trsil.org/employers/retirement-issues/post-retirement-limitations for more details.

- All of the time that a teacher or administrator is required to be present for licensed duties is subject to the limitations. For teachers, this includes preparation periods and time before, between and after classes. For administrators, this includes attendance at school board meetings. Extra duties that do not require a teaching license are not subject to the post-retirement limits.

- The same post-retirement employment limits apply to retired TRS members employed by school districts or private entities.

- If you are retired under the Illinois Retirement Systems Reciprocal Act, you must adhere to the post-retirement limitations of each system under which you retired.

- You may be employed by a public school district without limitation in a position not covered by TRS, such as teacher’s aide or as a bus driver if you didn’t retire under the Reciprocal Act.

- You may be employed by a college, university or private school without limitation if you didn’t retire under the Reciprocal Act.

- If you exceed the TRS post-retirement limits after being retired for one complete school year:

- TRS must be notified.

- Your retirement benefit will be suspended, including any reciprocal retirement.

- You will re-enter active membership.

- Your employer must remit TRS contributions for you on all creditable earnings after the employment limits are exceeded.

- Your state health insurance coverage will be canceled, effective on the first of the month following your re-entry into active service.

TRS Receives Awards for Financial Reporting and Plan Administration

Certificate of Achievement for Excellence in Financial Reporting

The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to TRS for its Comprehensive Annual Financial Report for the fiscal year ended June 30, 2016. This was the 28th consecutive year that the System has achieved this prestigious award. In order to be awarded a Certificate of Achievement, a government or government entity must publish an easily readable and efficiently organized Comprehensive Annual Financial Report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current Comprehensive Annual Financial Report continues to meet the Certificate of Achievement Program’s requirements, and we are submitting it to the GFOA to determine its eligibility for another certificate.

Public Pension Coordinating Council (PPCC) Recognition Award for Administration

TRS received the Recognition Award for Administration in 2017 in recognition of meeting professional standards for plan administration as set forth in the Public Pension Standards of the PPCC. The award is presented by the PPCC, a confederation of the National Association of State Retirement Administrators (NASRA), the National Conference on Public Employee Retirement Systems (NCPERS) and the National Council on Teacher Retirement (NCTR).

Early 2018 Important Retirees Tax and Payment Reminders

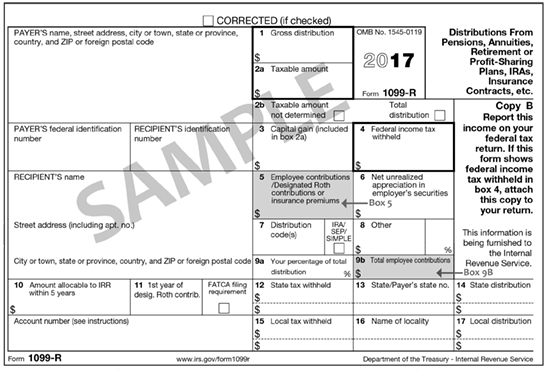

Expect arrival of 1099-R

If you received a TRS benefit in 2017, the Office of the Comptroller will mail an IRS Form 1099-R to you by

Jan. 31, 2018. This form will report your income received from TRS during 2017.

The amount shown in Box 5 on the 1099-R form represents the non-taxable portion of TRS retirement benefits paid to you for the year (see graphic below) and is the difference between Boxes 1 and 2a. Box 5 does not represent the amount of your TRIP premiums for 2017. Box 9B will only have a value if 2017 was the first year that you received a benefit from TRS.

If you do not receive a 1099-R form by Feb. 15, 2018 or you need a duplicate copy sent to you, please log in to the secure Member Account Access area. Annually after Feb. 1, you may request a duplicate 1099-R online for a prior year. Duplicates are mailed by the Illinois Comptroller’s Office.

If you have not yet set up your online member account, please watch this video to learn how: https://www.trsil.org/videos/accessing-your-trs-member-account-online. Your member ID is required to set up an account.

Annual increase reflected on Feb. 1 check because it is your payment for January

TRS pays your monthly benefit in arrears. The check issued Jan. 1, 2018 is your payment for the month of December 2017. Cost-of-living adjustment (COLA) increases, certain insurance premiums and federal tax withholding changes will be reflected on the check issued Feb. 1, 2018, which is your monthly annuity for January 2018.

The annual 3 percent COLA will be reflected on your Feb. 1, 2018 check. With some exceptions, recipients of monthly survivor benefits will also see a 3 percent increase. The COLA increase is first effective on Jan. 1 following either your first retirement anniversary or your 61st birthday, whichever is later. TRS only sends a notification letter before your first COLA occurs. Retirees may log in to the secure Member Account Access area to view their monthly and annual earnings statements.

Federal income tax withholding tables update

Revised federal income tax withholding tables did not go into effect on Jan. 1, 2018. As a result, the federal taxes withheld from your Jan. 1, 2018 annuity payment will remain the same unless changes were made to your record. TRS is awaiting further direction from the State of Illinois Office of the Comptroller and the Internal Revenue Service. Future updates about federal withholding will be posted to our website as information becomes available.

TRS cannot give tax advice. You may wish to contact a qualified tax advisor or the Internal Revenue Service at (800) 829-1040 to ensure that you have adequate federal withholding for the 2018 tax year. If you are underwithholding, there could be a negative consequence at tax time.

If you would like to change your withholding election, you must complete a new Form W4-P. You may print a personalized Form W4-P online within the secure Member Account Access area after you have signed in. Or, you may call your local Internal Revenue Service office for a blank form or download the blank form from the IRS website: http://www.irs.gov/pub/irs-pdf/fw4p.pdf. A new Form W4-P replaces any former withholding on file with TRS.

TRS Loses Two Dedicated Colleagues in 2017

Vickie Geiger

6/20/1961–1/13/2017

At TRS, 2017 began and ended with sadness as we mourned the loss of two valued colleagues who were dedicated to our members and the System’s mission during their careers.

Vickie joined TRS in 1988 as an Employer Services Department auditor. She was known throughout TRS as a hard worker who was always willing to go the extra mile for TRS members.

Vickie was outspoken, caring and selfless. She was full of vitality and always focused on the best for her department, her friends, her family and especially the lights of her life – her sons Billy and Timmy.

Although Vickie’s two-year battle with cancer was difficult, her strength and perseverance were an inspiration to everyone around her.

She is missed as a valued and respected member of the TRS family.

John Brillhart

11/17/1972–11/6/2017

John joined TRS in 2006 as a member services representative and he helped members navigate the ins-and-outs of TRS and their retirements every day. Always a “team player,” John shared his expertise with genuine sincerity and humility.

Known for his easy-going nature, kind heart and great sense of humor, he would go out of his way to make someone smile. John was a wonderful friend and father, and more than anything else he treasured time with his two daughters, Sadie and Cora.

Throughout Central Illinois, John was well-known for his love of music. He sang and played guitar for many years and often shared his talents with family, friends and coworkers.

John’s sudden death in a single-car accident had a profound effect on TRS. His humor and caring spirit are greatly missed.