Executive Director’s Message: Optimistic About the New Year

Welcome to 2019!

For TRS and its members, the new year is a blank page. We have no idea what will be written in the future, but our hope is that we will see words of support and encouragement that the retirement promises made to our members will be kept for a long, long time.

What was written last year contained good news and bad news for TRS. It’s good that the System earned 8.45 percent on its investments during the last fiscal year, collected more than $9 billion in revenue and paid out $6.5 billion to its members. It’s good that for the last 40 years our investment return, at 9.2 percent, has exceeded our expectations of 7 percent. For the foreseeable future, TRS is stable and all benefits will continue to be paid on time.

The bad news is that the long-term financial problems that the System deals with on a perpetual basis are still with us. While TRS currently has $51 billion in assets, it carries a $75 billion long-term unfunded liability caused by decades of state government underfunding. That unfunded debt grows every year because the state only pays about 60 percent of what is required to “fully fund” the System.

For the last few years, we have been able to maintain about 40 cents in assets for every $1 we should have in the trust fund. That’s not good and it’s a cause for concern because it leaves the future of TRS vulnerable to a downturn in the economy.

And that brings us back to the blank page and the direction state government will take in 2019 to address the financial problems of TRS and Illinois’ other public pension systems.

As we all know, there has been a sea change in the governor’s office – not only a new governor, but a new governor from a different party. There are many questions yet to be answered. What is Gov. Pritzker going to do differently from Gov. Rauner? What’s the new state budget going to look like? What is he going to do about the future of your pensions?

Looking back, the chronic financial challenges faced by TRS were amplified during the last four years. Political and policy differences between a Republican administration and Democratic legislature had a lot to do with that. It was unavoidable because the two parties have fundamentally different views of the role public pensions should play in society, as well as the solutions needed.

Looking forward, Democrats will be in control of both the legislative and executive branches of government. There still will be differences between the two major parties regarding the future of pensions. But I think we can safely say that with one party in charge, there will be less gridlock caused by those differences.

Our hope as we enter 2019 is that TRS can play a greater role in addressing our funding problems and writing any new public pension laws. In the past, both Democrats and Republicans have unfortunately operated under “ready, shoot, aim” rules. For instance, instead of creating a Tier 3 benefit that can’t be implemented because the new language is incompatible with existing statutes, maybe with our input up-front things could have been done right on the first go-around.

Just as we were always willing to work cooperatively with the previous administration to develop workable solutions to the state’s pension problems, TRS will start the new year with the same offer and attitude toward the incoming governor.

This is an opportunity to work with the governor’s office and the General Assembly to help fill in the first blank page of 2019 with more good news – and better safeguard the retirement promises made to our members for generations to come.

Best Wishes,

Dick Ingram

TRS Executive Director

Two “Buyout” Programs for Members Available in 2019

A voluntary “accelerated annual increase” program for retiring Tier 1 members began in January and TRS continues to make steady progress on implementing a separate “buyout” program for eligible inactive members in spring 2019.

The law authorizing both buyout programs was approved last year and is designed to help reduce the System’s total long-term pension liability. The programs will automatically sunset on June 30, 2021.

Tier 1 “Accelerated Annual Increase” (AAI)

For the next two years, when a Tier 1 member informs TRS that he/she wants to retire, TRS will ask whether the member has any interest in participating in what is being called the “Accelerated Annual Increase” program, or “AAI.” If a member is interested, the program will be explained and he/she will be given an estimate of the AAI payment and a formal election form.

Armed with this basic information, members will have to make an irrevocable decision on whether to participate in the AAI program or not before the rest of the retirement process can continue. TRS strongly suggests that members considering the AAI program seek the advice of a trusted financial planner before making a final decision.

All Tier 1 members accepting the AAI will:

- Renounce their rights to the current Tier 1 Annual Increase – which is a 3 percent rise in their pension benefits that always is calculated from the amount of their current pensions.

- Accept a new annual increase – a 1.5 percent rise in their pensions that always is calculated from the original amount of their benefits.

- Receive a lump-sum “accelerated pension benefit payment” that equals 70 percent of the monetary difference between the estimated lifetime value of the old 3 percent annual increase and the estimated lifetime value of the new 1.5 percent annual increase.

For members who accept the AAI, their new 1.5 percent increases will take effect on the Jan. 1 following their 67th birthdays, or after the first anniversary of their retirements, whichever is later. The 3 percent Tier 1 increase will continue to take effect on the Jan. 1 following a member’s 61st birthday or after the first anniversary of their retirements, whichever is later.

Inactive Member Buyout

Inactive members in both Tier 1 and Tier 2 may be eligible for this program. The buyout amount will equal 60 percent of the present value of the member’s anticipated pension benefits. In return, a member who accepts the buyout will give up any future rights to a reoccurring TRS benefit when they get older.

To be eligible, an inactive member must have “accrued sufficient service credit to be eligible to receive a retirement annuity” at some point in the future when other eligibility criteria are met. An inactive Tier 1 member must have at least five years of TRS service. An inactive Tier 2 member must have at least 10 years of TRS service.

Currently, approximately 20,000 TRS members are eligible for this accelerated payment, out of a total of 131,812 inactive members.

TRS will notify all eligible inactive members in 2019 when they can apply for the buyout. At that time, TRS will provide an estimate of how much the member will receive through the buyout program. A member’s decision to participate or not participate is irrevocable.

Inactive members cannot add service credit from another public pension system to their TRS service in order to meet the eligibility requirement for a TRS benefit that would make them eligible for a buyout. If an inactive member accepts the buyout, he/she cannot pay the buyout back to TRS later in order to re-establish past service. And if an inactive member accepts the buyout and he/she returns to active TRS service, his/her new service credit starts accumulating on the day they return to active service.

Payments Not Guaranteed

All members joining either program will be able to receive their AAI payments as cash or as a “rollover” into a private tax-qualified retirement plan. If a member takes the payment as cash, it will be subject to all applicable federal taxes and charges, as well as any involuntary garnishments by the state or federal government, such as unpaid student loans.

Agreeing to participate in the Accelerated Annual Increase (AAI) Program does not guarantee payment.

TRS is not responsible for funding the AAI Program. No TRS funds will be used to pay the accelerated benefits.

Under state law, funding for the AAI Program is generated solely by the sale of up to $1 billion in state bonds. The sale of these bonds is the responsibility of the Governor’s Office of Management and Budget.

TRS cannot predict when these bonds will be sold or when AAI participants will receive their one-time payments.

Once the state issues the bonds and the funds are available they will be distributed to applicants on a first-come, first-served basis. That means it is possible that your application may not be funded if the demand for funds is greater than the amount of money generated by the bond sale.

TRS Board of Trustees Election to Be Held May 1, 2019

Candidate Petitions to Be Filed in January

TRS will hold an election on May 1, 2019 for two active teacher trustees and one annuitant trustee to serve on the Board of Trustees for 4-year terms beginning July 15, 2019.

The election is conducted in accordance with the Illinois Pension Code and our board election rules. Petition forms and instructions for nominating trustee candidates are available on the website. Petitions must be filed with the System Jan. 1 - 30.

Electronic voting for the nominated candidates will be available April 1 through 10 a.m. on May 1. To vote by electronic ballot, please ensure we have your valid email address on file. Paper ballots will only be mailed if we do not have your email address or you request a paper ballot.

Please see our next newsletter for candidate profiles and more details about the election process.

Upcoming Board Meeting Dates

Unless otherwise indicated on the TRS website, meetings will be held at the TRS Springfield office, 2815 W. Washington St., Springfield, Illinois. This schedule is subject to change. Board actions can be found online under the TRS Board of Trustees minutes pages.

- March 14-15, 2019: Springfield

- April 25-26, 2019: Rosemont, Hyatt Regency O’Hare, 9300 W. Bryn Mawr Ave.

- June 13-14, 2019: Springfield

Employer Pay-period Reporting is Key to Major Initiatives

The implementation of two major changes in the Illinois Pension Code depends on a successful conversion of how often employers report member data to TRS. Instead of annual reports, TRS will move to a reporting schedule based on each school district’s pay periods.

TRS staff are currently developing the new pay-period reporting system and have engaged a “pilot” group of 30 school districts from throughout the state that will work with TRS during development. Based on the current progress, we expect the new system to be operational in July 2020.

Pay-period reporting is a vital first step in carrying out two legislative mandates:

- New Defined Contribution (DC) Benefit – A new law approved in 2018 requires TRS to set up, for the first time, a voluntary defined contribution retirement plan for active members. It is impossible to administer a DC plan if member contributions are only reported on an annual basis.

- Tier 3 – One of the major parts of the pending Tier 3 benefit structure is a DC plan for all of its members that works in conjunction with a pension component. Again, TRS cannot administer the Tier 3 DC portion without pay-period reporting.

TRS Receives Awards for Financial Reporting and Plan Administration

Certificate of Achievement for Excellence in Financial Reporting

The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to TRS for its Comprehensive Annual Financial Report for the fiscal year ended June 30, 2017. This was the 29th consecutive year that the System has achieved this prestigious award. In order to be awarded a Certificate of Achievement, a government or government entity must publish an easily readable and efficiently organized Comprehensive Annual Financial Report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current Comprehensive Annual Financial Report continues to meet the Certificate of Achievement Program’s requirements, and we are submitting it to the GFOA to determine its eligibility for another certificate.

Public Pension Coordinating Council (PPCC) Recognition Award for Administration

TRS received the Recognition Award for Administration in 2018 in recognition of meeting professional standards for plan administration as set forth in the Public Pension Standards of the PPCC. The award is presented by the PPCC, a confederation of the National Association of State Retirement Administrators (NASRA), the National Conference on Public Employee Retirement Systems (NCPERS) and the National Council on Teacher Retirement (NCTR).

Early 2019 Important Retirees Tax and Payment Reminders

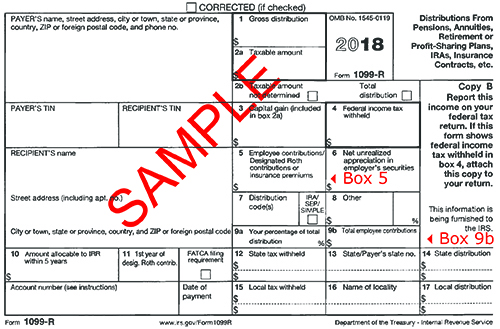

Expect arrival of 1099-R

If you received a TRS benefit in 2018, the Office of the Comptroller will mail an IRS Form 1099-R to you by

Jan. 31, 2019. This form will report your income received from TRS during 2018.

The amount shown in Box 5 on the 1099-R form represents the non-taxable portion of TRS retirement benefits paid to you for the year (see graphic below) and is the difference between Boxes 1 and 2a. Box 5 does not represent the amount of your TRIP premiums for 2018. Box 9B will only have a value if 2018 was the first year that you received a benefit from TRS.

If you do not receive a 1099-R form by Feb. 15, 2019 or you need a duplicate copy sent to you, please log in to the secure Member Account Access area on the TRS website. Annually after Feb. 15, you may request a duplicate 1099-R online for a prior year. A duplicate is mailed by the Illinois Comptroller’s Office and will take up to 10 business days for you to receive it.

If you have not yet set up your online member account, please watch this video to learn how: https://www.trsil.org/videos/accessing-your-trs-member-account-online. Your Member ID is required to set up an account.

Annual increase reflected on Feb. 1 check because it is your payment for January

TRS pays your monthly benefit in arrears. The check issued Jan. 1, 2019 is your payment for the month of December 2018. Cost-of-living adjustment (COLA) increases, certain insurance premiums and federal tax withholding changes will be reflected on the check issued Feb. 1, 2019, which is your monthly annuity for January 2019.

The annual 3 percent COLA will be reflected on your Feb. 1, 2019 check. With some exceptions, recipients of monthly survivor benefits will also see a 3 percent increase. The COLA increase is first effective on Jan. 1 following either your first retirement anniversary or your 61st birthday, whichever is later. TRS only sends a notification letter before your first COLA occurs. Retirees may log in to the secure Member Account Access area to view their monthly and annual earnings statements.

Tax withholding tables changed

Revised federal income tax withholding tables went into effect on Jan. 1, 2019. As a result, the federal taxes withheld from your Jan. 1, 2019 annuity payment may increase or decrease based on your filing status.

TRS cannot give tax advice. You may wish to contact a qualified tax advisor or the Internal Revenue Service at (800) 829-1040 to ensure that you have adequate federal withholding for the 2019 tax year. If you are underwithholding, there could be a negative consequence at tax time.

If you would like to change your withholding election, you must complete a new Form W4-P. You may print a personalized Form W4-P online within the secure Member Account Access area after you have signed in. Or, you may call your local Internal Revenue Service office for a blank form or download the blank form from the IRS website: http://www.irs.gov/pub/irs-pdf/fw4p.pdf. A new Form W4-P replaces any former withholding on file with TRS.

TRS Benefits Report Available Online for Active and Inactive Members

In late November, active and inactive members were emailed that their 2018 TRS Benefits Reports were available for viewing online on the TRS website.

Reports are only sent to members who are not yet collecting a benefit. Retirees do not receive TRS Benefits Reports. The report summarizes the following information about a member’s TRS account: service credit, refundable contributions, beneficiary refund, beneficiaries, sick leave service, and 2.2 upgrade information.

If you are an active or inactive member who has not provided your email address to TRS and you received this newsletter by mail, please visit https://www.trsil.org. Select “Member Login” on the home page to begin creating your online account. You will need your Member ID. If you do not know it, call us at 877-927-5877 (877-9-ASK-TRS). You will be able to view your TRS Benefits Report after signing in.

Additionally, please enter your email address under the contact information in the secure area so you will receive future emails from us.

Recent payments and changes in outstanding balances will not be reflected on your report, but will be shown in your online account. If you need to change your beneficiaries, complete a Member Information and Beneficiary Designation (MIBD) form: https://www.trsil.org/MIBD_form. Please print out and mail the form to us and we will update your file. A new MIBD form replaces any former version on file with TRS. If you see an error on your reported service record or salaries, contact your employer (school district) without delay to correct the problem. This information is reported by your employer on your behalf to TRS. It may be more difficult to correct an error if you wait until retirement.

Please call us if you believe your report has an error (other than salary or service credit), if you need an additional copy or if you have any questions about the content.

Post-Retirement Employment Limitations Apply to All Retirees

Now that the school year is halfway over, all retired members who substitute teach should refresh themselves about the limitations before problems arise.

It is the responsibility of all retired teachers to observe all post-retirement limitations. TRS will suspend a retired teacher’s benefit if the teacher exceeds the limitations.

For post-retirement employment purposes, the Illinois Pension Code says one full day of service is equal to five hours. Read https://www.trsil.org/employers/retirement-issues/post-retirement-limitations for more details.

You must follow the post-retirement work limitations set in state law:

- Following your retirement, you may not resume employment in a TRS-covered position, including substitute and summer school teaching, in the same school year in which you last contributed to TRS. The official school year is July 1 through June 30. If you retire during the school year, you may teach summer school only if the first day of that teaching service is after June 30. In addition, you must wait 30 days from the effective date of your resignation before performing any post-retirement teaching for the same employer.

- In the school year following the school year in which you last contributed to TRS, you may be employed in a TRS-covered position for up to 120 paid days or 600 paid hours per school year and still receive your TRS annuity/benefit. The 120 days/600 hours limit is in effect through June 30, 2020. Only work that requires teacher licensure is subject to these limitations.

- If you resume TRS-covered employment in the same school year that you last contributed to TRS as an active member, you must repay all annuity payments received from the day of retirement.

- All of the time that a teacher or administrator is required to be present for licensed duties is subject to the limitations. For teachers, this includes preparation periods and time before, between and after classes. For administrators, this includes attendance at school board meetings. Extra duties that do not require a teaching license are not subject to the post-retirement limits.

- The same post-retirement employment limits apply to retired TRS members employed by school districts or private entities.

- If your preretirement job no longer requires teacher licensure due to a change in job title or a minor change in job duties, the work is subject to the termination of service requirements and the post-retirement limitations.

- If you are retired under the Illinois Retirement Systems Reciprocal Act, you must adhere to the post-retirement limitations of each system under which you retired.

- You may be employed by a public school district without limitation in a position not covered by TRS, such as teacher’s aide or as a bus driver, if you didn’t retire under the Reciprocal Act.

- You may be employed by a college, university or private school without limitation if you didn’t retire under the Reciprocal Act.

- If you exceed the TRS post-retirement limits after being retired for one complete school year:

- TRS must be notified.

- Your retirement benefit will be suspended, including any reciprocal retirement.

- You will re-enter active membership.

- Your employer must remit TRS contributions for you on all creditable earnings after the employment limits are exceeded.

- Your state health insurance coverage will be canceled, effective on the first of the month following your re-entry into active service.

- If you exceed the TRS post-retirement limits within the first year of retirement, all annuity payments must be repaid.