TRS Members Start Joining New Supplemental Savings Plan

Bring More to your future. The new TRS Supplemental Savings Plan (SSP) is open for business!

Bring More to your future. The new TRS Supplemental Savings Plan (SSP) is open for business!

In early January, the first eligible TRS members signed up to participate in the SSP, the System’s first-ever defined contribution (DC) salary deferral plan. These members will begin making contributions to their new SSP accounts in March 2022.

The SSP allows participants to dedicate a portion of every paycheck to a 457(b) deferred compensation savings plan administered by Voya Financial, of New York, a national leader in retirement security for millions of Americans.

When SSP participants retire and start to receive their monthly pensions, they also will be able to draw on the money they’ve saved in their SSP accounts.

The SSP is completely voluntary on the part of eligible active members in Tier 1 and Tier 2. The SSP will not replace the pension of any TRS member.

SSP participants will be able to choose how to invest their accounts for the goal of helping them grow for their future needs. Voya will administer all SSP accounts while TRS will continue to oversee each participant’s defined benefit (DB) pension.

The SSP has been in development since 2018, when the General Assembly enacted a law that requires TRS and the state’s major public retirement systems to create compatible DC plans to supplement the existing DB pension plans.

TRS has worked diligently to create a best-in-class DC plan that will provide members the means to Bring More to their future retirements. Here’s a quick overview:

Who can participate?

Active TRS members who are full-time and part-time contractual employees are eligible for the SSP. A TRS employer must adopt the SSP for their employees to be eligible to participate. Retired and inactive TRS members are not eligible for the SSP.

How can I find out more about the SSP and register?

Interested TRS members who are eligible to participate are encouraged to visit the TRS SSP participant website at trsilssp.voya.com. Members who enroll in the SSP will see contributions deducted from their paychecks beginning in March 2022.

Your SSP account

Participating TRS members can access their accounts online through the TRS SSP participant website at trsilssp.voya.com or via the toll-free TRS SSP Service Center at 844-877-4572 (844-TRS-457B).

Why Bring More with the SSP?

Reason 1: Your future is in your hands.

The truth is we all have to take responsibility for our future and that includes making sure we have the income we’ll need in retirement. Your pension may not cover your entire retirement, so funding the rest of your retirement paycheck is up to you through personal savings and other retirement income sources — including an optional retirement savings plan such as the SSP. By contributing to the SSP, you’ll be taking a great step toward building your savings for tomorrow.

Reason 2: The sooner you start, the more you could have in retirement.

Starting early can make a huge difference. The longer you save, the more you will save and the more time your savings will have to potentially grow — through investment returns that go back into your account where they can earn more, which is referred to as compounding.

Your SSP contributions

The SSP offers you the opportunity to save with pre-tax and/or Roth after-tax contributions. You can choose either or both. Pre-tax contributions are taken from your pay before any taxes are deducted. The payment of taxes is deferred until you withdraw the money from your account. Roth after-tax contributions are taken from your pay after taxes have been deducted. These contributions and any qualifying earnings are tax free upon withdrawal.

You can elect the amount you want to contribute per paycheck to your SSP account (in whole dollar increments). You must contribute a minimum of $30 per pay period. An annual IRS dollar limit applies to the total amount you can contribute to the SSP each year. To learn more about the IRS contribution limits visit www.voya.com/IRSlimits.

You can change your contribution rate at any time. In addition, you can elect the Automatic Rate Escalator feature which automatically increases your contributions based on the amount and timing you elect.

Your SSP investment decisions

When you enroll in the SSP, you will be asked to choose how your contributions will be invested. Choosing an investment strategy that aligns with your goals, risk tolerance and time horizon is a key part of meeting your future retirement needs.

For some, the process of selecting investments can be intimidating either because they prefer investments to be selected for them or feel they do not have adequate time or resources to review the options.

Others prefer to manage their own investments. The SSP investment menu has been designed to accommodate these different types of investors and provide you the information you need to feel confident in your investment choices.

You can choose to invest in any mix of the options made available by TRS and can change your investment elections and/or balances at any time.

The SSP offers a diverse array of investment options and detailed information for each, including risk and return characteristics. You should evaluate each fund’s performance carefully and consider whether you are comfortable with the degree of risk. Past performance is not a guarantee of future results. No investment is insured or guaranteed by any government agency.

You are responsible for any losses that result from your investment choices. TRS and your employer are not responsible for any losses. TRS, your employer and Voya Financial are not authorized to give you investment advice.

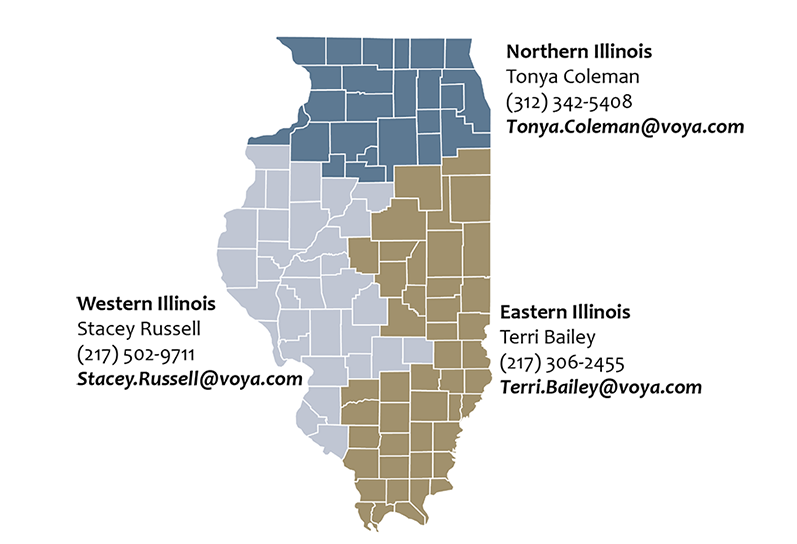

Connect with a Local TRS SSP Representative

Bring More to your retirement plans with the SSP. TRS and Voya have three representatives to specifically help eligible members learn more about the SSP. Note that a representative cannot give investment advice or monitor member accounts.

Your local TRS SSP representative will provide ongoing support to help meet your needs, including:

- SSP information and enrollment assistance

- Consolidation of retirement accounts

To schedule a virtual appointment with a local representative, go to https://trsssp457b.timetap.com.

Trustee Matthew Hunt Named TRS Board President; Blackburn Appointed

In August, Gov. JB Pritzker appointed Trustee Matthew Hunt, of Glen Ellyn, as president of the Board of Trustees. He succeeds former Trustee Devon Bruce, of Lake Forest, who resigned after 18 months as Board president.

President Hunt has served as a Trustee since June of 2019. He is vice president of Hunt Insurance Agency, Inc., in Palos Heights, an independent, family-owned agency established in 1957. He is a graduate of Creighton University with a B.S. in economics. Prior to joining the TRS Board, President Hunt served as a member of a municipal police pension fund and as a member of the Illinois State Elevator Safety Review Board.

In September, Gov. Pritzker appointed Will County Auditor Kevin “Duffy” Blackburn as the System’s newest trustee.

Trustee Blackburn is serving his fourth term as the elected county auditor. He is responsible for auditing claims against the county, government expenses and analyzing and preserving official statistical and financial information. He also serves as an adjunct professor at Benedictine University in Lisle, Joliet Junior College and the University of St. Francis in Joliet.

Trustee Blackburn earned a master’s degree in accounting and finance management and a master’s degree in business administration from the Keller Graduate School of Management at DeVry University and a bachelor’s degree in economics from the University of Iowa.

New Laws Affecting Members Enacted in 2021

Last year, Gov. JB Pritzker signed a number of new laws affecting TRS and its members, including three new measures designed to help correct the unforeseen effects on teachers of the COVID-19 school lockdown and remote learning.

Last year, Gov. JB Pritzker signed a number of new laws affecting TRS and its members, including three new measures designed to help correct the unforeseen effects on teachers of the COVID-19 school lockdown and remote learning.

Public Act 102-0016 removes the requirement that the final average salary calculation use the four “consecutive” highest salaries for Tier 1 members or the eight “consecutive” highest salaries for Tier 2 members. This change only applies to members who are retiring after June 1, 2021 and the 2020-21 school year is used in their final average salary calculations. For a member retiring on or after June 1, 2021 and for whom the 2020-21 school year is used in the final average salary calculation, the final average salary will be based on the four highest years within the last 10 years of creditable service for Tier 1 members or eight highest years within the last 10 years of creditable service for Tier 2 members. This could impact employer contributions due for salary increases in excess of 6 percent.

Public Acts 102-0525 and 102-0016 create new exemptions from a requirement that school districts pay a higher contribution to TRS if they grant a raise to a TRS member on the verge of retirement that is greater than 6 percent from one year to the next. The exemptions are designed to eliminate higher year-to-year salaries inadvertently caused by the COVID-19 lockdown and remote learning.

The exemptions are for:

- Overload or stipend work performed in a school year subsequent to a school year in which the employer was unable to offer or allow overload work or stipend work due to an emergency declaration limiting such activities. These exemptions would be applicable if the 2020-21 and/or 2021-22 school years are used in the calculation of a retiree’s final average salary calculation.

- Increased instructional time during the 2020-21 school year.

- Summer school teaching between May 1, 2021 and Sept. 15, 2022.

Public Act 102-0525 allows TRS members a temporary opportunity to “establish optional credit for up to 2 years of service as a teacher or administrator employed by a private school recognized by the Illinois State Board of Education…” The teacher must have been certified or licensed by the ISBE while working for the private school, must have at least 10 years of TRS service credit and must pay the applicable member contribution for the private school time.

Public Act 102-0440 extends the life of the “subject shortage area” statute to June 30, 2024. With the approval of their regional school superintendent, school officials can declare that they have a shortage of qualified teachers in a particular subject and can hire retired teachers to fill those vacancies. Those retired teachers do not lose their pension benefits.

Public Act 102-0537 extends the “sunset” date for increased post-retirement work limits to June 30, 2023. A retired TRS member will not lose her/his pension benefit if she/he teaches for up to 120 days or 600 hours during a single school year. The law is designed to help address the chronic teacher shortage in Illinois.

Public Act 102-0540 requires TRS to “automatically enroll” all “new” TRS members in the Supplemental Savings Plan. Auto-enrolled members can “opt out” of the SSP within 90 days of their first day of employment. All existing active TRS members will have the option of joining the SSP and will not be automatically enrolled.

Members Should Be Alert for Potential Scams

TRS is encouraging members to remain alert and vigilant for potential cybercrimes and scams that target the benefit payments of retirees.

TRS is encouraging members to remain alert and vigilant for potential cybercrimes and scams that target the benefit payments of retirees.

The System is always on high alert for cybercriminals and scams that affect TRS retirees.

You can do your part by carefully scrutinizing unsolicited mail, telephone calls or emails that suggest they have some connection to TRS, but in reality they do not.

If you are in the least bit suspicious about something you receive that purports to enhance or better manage your benefit, always contact TRS to check on the veracity of the communication or offer before speaking or meeting with anyone who claims to have information about your TRS benefits.

TRS and law enforcement officials across the state recently have noticed an uptick in scams aimed at retired school and government workers, the elderly and others considered vulnerable by con artists and cybercriminals.

The increase in activity could be due to a number of factors, including the onset of income tax season, an increased dependency on the use of the internet due to COVID-19 and a general uncertainty about the economy.

As you remain vigilant against crime and scams, here are a few things to remember:

- TRS will never call you or contact you through the mail or in an email to endorse any company’s product or service relating to your pension, health insurance or another benefit.

- Always carefully guard your personal information. Don’t share.

- Be wary of all links and attachments in unsolicited emails.

- Don’t be rushed into making any decision.

- Independently verify the identity of the person or company contacting you.

- TRS is monitoring the internet and other forms of communication to spot trends and potential unauthorized activity directed at its members. Members may help secure this intelligence safety net by contacting Member Services with tips about activities they find suspicious.

TRS will take appropriate action when we become aware of individuals or businesses using misleading tactics to give a false impression that they are affiliated with TRS.

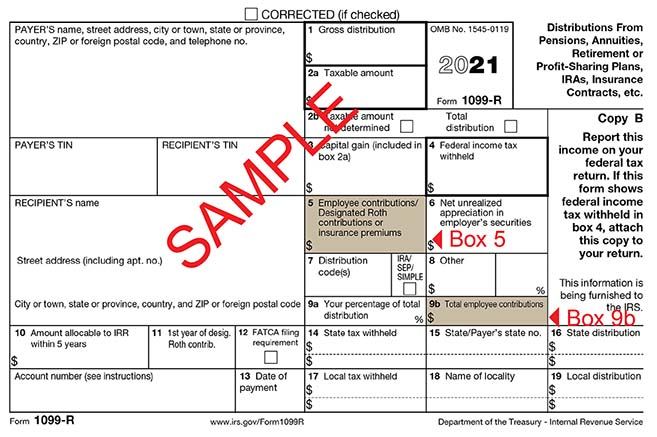

Early 2022 Important Tax Reminder for TRS Retirees

Expect arrival of 1099-R

If you received a TRS benefit in 2021, the Office of the Comptroller will mail an IRS Form 1099-R to you by Jan. 31, 2022. This form will report your income received from TRS during 2021.

The amount shown in Box 5 on the 1099-R form represents the non-taxable portion of TRS retirement benefits paid to you for the year (see graphic below) and is the difference between Boxes 1 and 2a. Box 5 does not represent the amount of your TRIP premiums for 2021. Box 9B will only have a value if 2021 was the first year that you received a benefit from TRS.

If you do not receive a 1099-R form by Feb. 16, 2022 or you need a duplicate copy sent to you, please log in to the secure Member Account Access area on the TRS website. After Feb. 16, you may request a duplicate 1099-R online for a prior year. A duplicate is mailed by the Illinois Comptroller’s Office and it will take up to 10 business days for you to receive.

If you have not yet set up your online member account, please watch this video to learn how: trsil.org/videos/accessing-your-trs-member-account-online. Your Member ID is required to set up an account.

Purchasing Private School Service Credit

If you previously worked in a recognized private school, you may be eligible to purchase up to two years of service credit. Call us at (877) 927-5877, Monday through Friday, 8:30 am to 4:30 pm, to request a Recognized Illinois Non-public Service Certification form. Retired members are not eligible for this credit.

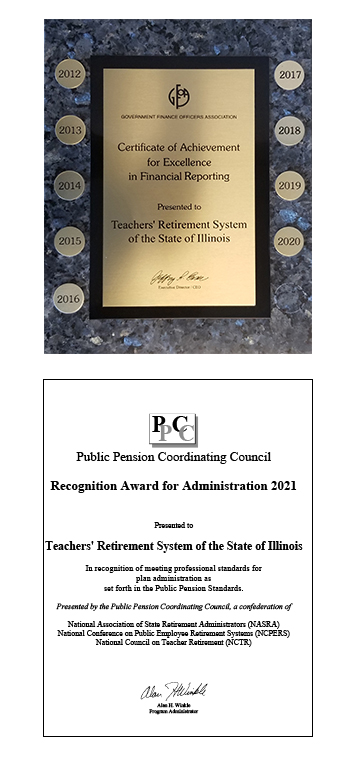

TRS Receives Awards for Financial Reporting and Plan Administration

Certificate of Achievement for Excellence in Financial Reporting

The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to TRS for its Comprehensive Annual Financial Report for the fiscal year ended June 30, 2020. This was the 32nd consecutive year that the System has achieved this prestigious award. In order to be awarded a Certificate of Achievement, a government or government entity must publish an easily readable and efficiently organized Comprehensive Annual Financial Report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our fiscal year 2021 Comprehensive Annual Financial Report continues to meet the Certificate of Achievement Program’s requirements, and we are submitting it to the GFOA to determine its eligibility for another certificate.

Public Pension Coordinating Council (PPCC) Recognition Award for Administration

TRS received the Recognition Award for Administration in 2021 in recognition of meeting professional standards for plan administration as set forth in the Public Pension Standards of the PPCC. The award is presented by the PPCC, a confederation of the National Association of State Retirement Administrators (NASRA), the National Conference on Public Employee Retirement Systems (NCPERS) and the National Council on Teacher Retirement (NCTR).

TRS Finances Improve During 2021; Investments Reach Record Levels

By every vital measurement, TRS finances improved during 2021.

- TRS managed $63.9 billion in investments at the end of fiscal year 2021 – a record for the System. That’s an increase of $12.4 billion in investments over the previous year, or a 24.1 percent climb.

- By the end of December 2021, TRS investments surpassed $65.0 billion.

- The TRS portfolio investment return in fiscal year 2021 was a positive 25.5 percent, net of fees.

- The 40-year investment return for TRS at the end of fiscal year 2021 was 9.5 percent, net of fees.

- After several years of hovering at 40 percent, the System’s long-term funded ratio improved to 42.5 percent.

Through careful planning, the TRS Investment Department successfully navigated the perils of the COVID-19 pandemic’s attack on the economy. All public pension systems lost money initially during the first months of the pandemic. But compared to similar public pension systems, TRS ranked among the nation’s leaders in its ability to preserve assets, which set up a remarkable rebound over the next 18 months. Total TRS assets grew from a low of $48.5 billion in March 2020 at the beginning of the pandemic to over $65 billion by the 2021 calendar year end.

TRS maintains a focus on steady, long-term investment returns. The System recognizes that a majority of its members maintain relationships with TRS for decades. So even with the effects of the pandemic, the TRS long-term investment returns, at 9.5 percent, continued to exceed the System’s long-term assumed investment return of 7 percent.

The System’s strong investment returns and a stable funding commitment from state government over the last few years led to a slight decrease in the TRS unfunded liability from $80.7 billion to $79.9 billion.

“While a small step, the improvement in the funded ratio is a positive move toward bringing stability to the System’s long-term finances,” said TRS Executive Director Stan Rupnik. “Any improvement is good news for our members, but we all realize that there’s still a lot of work ahead of us to sustain this momentum and reach our goal.”

The funded ratio reflects the difference in the amount of money TRS has in assets against the amount of money the System needs to immediately pay all members the full amounts of benefits they are owed for the rest of time.

Altogether, the System’s fiscal year 2021 total long-term liability is $138.9 billion, a 2.4 percent increase over the previous year. While the funded ratio is important as an official measure of the System’s long-term fiscal health, it is not a reflection of the System’s current financial ability to pay benefits.

In any given year, TRS only is obligated under state law to pay out the amount of money owed annually to retired members and other beneficiaries. During fiscal year 2021, benefits owed totaled $7.4 billion. TRS was more than able to pay all benefits for the year on time and in full. In fact, for 82 years TRS has paid all benefits in full and on time.

Updated TRS Benefits Reports Online for Active and Inactive Members

In late November, active and inactive members were emailed that their TRS Benefits Reports from the past school year were available for viewing online on the TRS website.

Benefits Reports from the past school year were available for viewing online on the TRS website.

Reports are only sent to members who are not yet collecting a benefit. Retirees do not receive TRS Benefits Reports.

As a new feature this year, vested Tier 1 and Tier 2 members can view an estimate of their future retirement benefits. This estimate does not include any projected, reciprocal or pending service.

The report also summarizes the following information about a member’s TRS account: service credit, refundable contributions, beneficiary refund, beneficiaries, sick leave service and 2.2 upgrade information.

If you are an active or inactive member who has not provided your email address to TRS and you received this newsletter by mail, please visit trsil.org. Select “Member Login” on the home page to begin creating your online account. You will need your Member ID. If you do not know it, call us at 877-927-5877 (877-9-ASK-TRS). You will be able to view your TRS Benefits Report after signing in.

Additionally, please enter your email address under the contact information in the secure area so you will receive future emails from us.

Recent payments and changes in outstanding balances will not be reflected on your report, but will be shown in your online account.

If you need to change your beneficiaries, download your personalized Beneficiary Designation form by logging into your secure member account. Print out and mail the completed form or upload it online in the secure area and we will update your file.

A new Beneficiary Designation form replaces any former version on file with TRS.

If you see an error on your reported service record or salaries, contact your employer (school district) without delay to correct the problem. This information is reported by your employer on your behalf to TRS. It may be more difficult to correct an error if you wait until retirement.

Please call us if you believe your report has an error (other than salary or service credit), if you need an additional copy or if you have questions about the content.

Winter 2022. Published by the Teachers' Retirement System of the State of Illinois.