Gov. Pritzker Calls for $500 Million in “Extra” Funding for State Pensions

Gov. JB Pritzker’s call for $500 million in “above-and-beyond” state pension funding in fiscal years 2022 and 2023 leads the list of spring initiatives in the General Assembly that affect TRS, its members and stakeholders.

Gov. JB Pritzker’s call for $500 million in “above-and-beyond” state pension funding in fiscal years 2022 and 2023 leads the list of spring initiatives in the General Assembly that affect TRS, its members and stakeholders.

The governor’s plan to appropriate more money than the minimum requirement to Illinois’ public pensions has been praised by TRS leaders as a commitment to improve the retirement security of the state’s teachers.

“Governor Pritzker’s proposal to allocate a total of $19.5 billion to public pensions over two consecutive years reaffirms his strong partnership with generations of Illinois teachers,” said TRS Board President Matthew Hunt. “Since taking office, Gov. Pritzker has proven to be very supportive of our 432,000 members and their futures.”

Senate Bill 2803, which adds $300 million to the fiscal year 2022 state pension allocation of $9.4 billion, was approved in late March by the General Assembly and signed into law by Gov. Pritzker. The remaining $200 million in the governor’s pension funding plan will be added to the upcoming fiscal year 2023 state budget, which includes $9.6 billion for state pensions.

In his fiscal year 2023 state budget address, Gov. Pritzker said the added funds will reduce the future long-term liability of the state’s pension systems by an estimated $1.8 billion.

In fiscal year 2023, the state’s minimum statutory payment for TRS is $5.9 billion. It’s expected the payment to TRS will total $6.16 billion with the extra money.

The total long-term liability of the state’s five pension systems currently stands at $236.5 billion. The TRS unfunded liability is $80 billion.

This is the first time since 1994 that the state’s annual pension contribution will exceed the statutory minimum in two straight years.

Other TRS legislation of interest being considered by lawmakers this spring includes:

House Bill 1167 – Gov. Pritzker signed this bill that creates “COVID-19 paid administrative leave” time for TRS members who are fully vaccinated against the coronavirus. For TRS members who used sick time during the 2021-22 school year to deal with the coronavirus, the bill requires school districts to replace any “sick time” used for that purpose with the new COVID-19 administrative leave time. The sick time would be added back to a member’s accumulated sick leave “bank.”

House Bill 4292 – Allows state government to borrow up to $1 billion in additional money to continue funding the two public pension “accelerated benefit” programs. The state has borrowed $1 billion over the last two years to fund these member “buyouts.” The bill also extends the life of the two “buyout” programs until 2026. The original sunset date was June 30, 2024.

House Bill 5472 and Senate Bill 3201 – Expands the number of days during the 2021–2022 school year that retired TRS members can teach school full-time without that service negatively affecting the payment of their pensions. The current 120 days limit would be increased to 140 days. The bill also may extend the number of days during the 2022–2023 school year.

House Bill 5705 – Sets up the process that would require TRS and the state’s four other pension systems to divest money from Russian companies due to the country’s invasion of Ukraine. The bill calls on the Illinois Investment Policy Board to identify all potential Russian investment opportunities and place them on a “prohibited” list. TRS and the other pension systems would then have a set amount of time to pull all investments in those companies.

Senate Bill 932 – Makes it easier for state boards and commissions, including TRS, to substitute a virtual meeting for an in-person meeting due to potential health risks. The substitution would be at the discretion of the board chair or president.

Close Up: TRS Executive Management Spotlights

Over the last several years TRS has added or promoted new executives to manage the day-to-day operations of the System. Each of them brings extensive experience in their fields to the internal workings of TRS. Here are capsule biographies of the newer members of the System’s Executive Cabinet:

Deron Bertolo, Chief Financial Officer

Deron joined TRS in 2010 as director of investment accounting and was promoted to his current position in September 2020. Prior to TRS, Deron served for 20 years in various finance-accounting roles within the private sector. His previous employment includes controller positions with Honeywell and John Deere manufacturing facilities. He is a graduate of Eastern Illinois University in Charleston with a bachelor’s degree in finance.

Lori Dour, Acting Chief Benefits Officer

Lori joined TRS in 2003 as an internal auditor after working 10 years as an auditor and accounting manager in the private sector. Lori was promoted as the TRS claims manager in 2006 and to the deputy chief benefits officer in 2017. In that role, she was responsible for the administration of the annuitant payroll, insurance, benefits and member account processes. In July 2021, she was named acting chief benefits officer with additional responsibility over the implementation of the new TRS Supplemental Savings Plan as well as the System’s Counseling Services, Call Center and Outreach areas. Lori is a graduate of Illinois State University in Normal with a bachelor’s degree in accounting. She is a Certified Public Accountant.

Emily Peterson, General Counsel

Emily joined TRS in November 2021 from Horace Mann Educators in Springfield, where she served as vice president and assistant general counsel. At Horace Mann, she built extensive expertise on defined contribution plans. Between 2004 and 2010, Emily worked at the Illinois State Board of Investment (ISBI), as the plan’s general counsel and chief compliance officer. With ISBI, she acquired a universal understanding of the Illinois Pension Code, the legislative process and the fund’s investment program. After the ISBI, Emily served in private practice at Winston & Strawn in Chicago and with Sorling Northrup in Springfield. Emily holds a juris doctor degree from the Chicago-Kent College of Law and a bachelor’s degree from Eastern Illinois University in Charleston.

Jamie Stults, Director of Human Resources

Before joining TRS in April 2021, Jamie served as director, human resources business partner for Horace Mann Insurance Companies, based in Springfield. She held similar roles with the University of Chicago-Division of Specialized Care for Children and the Dominican Sisters of Springfield. Jamie holds a master’s degree in human resources management from Concordia University in St. Paul, Minnesota and a bachelor’s degree in business administration from Robert Morris College in Springfield. Jamie has acquired certifications as a Senior Professional in Human Resources and as a Society for Human Resources Management-Senior Certified Professional.

Christopher Wiedel, Director of Information Technology

A seven-year veteran of TRS, Chris was promoted to his current position in April 2020. During his tenure in IT administration, he has helped advance the strategic goals of TRS by implementing various cost-saving technical solutions. Before TRS, Chris was the information systems manager at the Sangamon County Sheriff’s Office.

Benefit Choice Period for Health Insurance Coverage Planned in May

The annual Benefit Choice Period for Teachers’ Retirement Insurance Program (TRIP) participants is planned for May 1-May 31, 2022. TRS will post any updates about the Benefit Choice Period on our website. Watch for the new Benefit Choice logo below on all Benefit Choice publications.

![]()

This open enrollment period is not for members currently enrolled in the State of Illinois Medicare Advantage Prescription Drug (MAPD) Plan-Total Retiree Advantage Illinois (TRAIL). The open enrollment period for TRAIL participants will be held in the fall.

Benefit Choice is the time to make changes in TRIP coverage and to enroll yourself and eligible dependents.

TRS members and their dependents who have previously opted out of the Teachers' Retirement Insurance Program (TRIP) can re-enroll in the program if they wish. Re-enrollment is allowed only during the annual open enrollment period.

The information about the Benefit Choice Period will be mailed to retirees currently enrolled in TRIP by the end of April.

The mailing will include an explanation of health insurance options for the coming fiscal year beginning July 1, 2022 and any upcoming changes in insurance benefits.

The full Benefit Choice booklet will be available at MyBenefits.illinois.gov.

If you already are enrolled in TRIP and wish to make a change in coverage, call MyBenefits Service Center (MBSC) at 844-251-1777 or log in at MyBenefits.illinois.gov. If you are enrolling yourself for the first time during the Benefit Choice Period, please contact TRS for a TRIP Participation Election form.

If you do not want to change your coverage, you do not have to do anything. Your current coverage will continue.

TRS does not administer TRIP. As a reminder, TRS determines eligibility, assists with enrolling members in the program and collects appropriate premiums. By law, CMS is the administrator that determines coverage benefits, establishes premiums, negotiates contracts with the insurance carriers, and resolves coverage and claim issues.

MBSC is the custom benefits solution service provider for CMS and can answer questions about changing coverage or electing benefits.

Keep Bank Information Current to Ensure Convenience of Direct Deposit

It is each member’s responsibility to keep her/his bank information current by notifying TRS when a banking change occurs. Banking changes include:

information current by notifying TRS when a banking change occurs. Banking changes include:

- changing a bank account number,

- changing a bank routing number,

- name change of bank,

- address change of bank and/or

- a merger with another banking entity.

Failure to notify TRS when a banking change occurs will result in the loss of direct deposit and the member will receive a paper benefit check. As a reminder, TRS members can update their bank information by printing a Direct Deposit form from the TRS website or by calling TRS to request a bank change form.

Interest in the TRS Supplemental Savings Plan Gains Momentum

The first months of activity for the new Supplemental Savings Plan (SSP) have revealed a growing interest in the voluntary savings plan designed to help TRS members Bring More to their futures.

The first months of activity for the new Supplemental Savings Plan (SSP) have revealed a growing interest in the voluntary savings plan designed to help TRS members Bring More to their futures.

Approximately 300 active members have signed up for this 457(b) deferred compensation savings plan. More than twice that number have expressed interest in the SSP and have requested more information or expressed interest in speaking with a representative from our partners at Voya Financial, of New York, to have their questions answered. Voya is a national leader in retirement security for millions of Americans.

While Voya will administer all SSP accounts, TRS will continue to oversee each participant’s defined benefit (DB) pension.

When SSP participants retire and start to receive their monthly TRS pensions, they also will be able to draw on the money they’ve saved in their SSP accounts. The SSP will not replace the pension of any TRS member.

As an SSP participant, you can elect the amount you want to contribute per paycheck (in whole dollar increments) but must contribute a minimum of $30 per pay period. You can change your contribution rate at any time. And you choose how to invest your money from any of the options made available by TRS. You can change your investment choices at any time.

Who can participate in the SSP?

Active TRS members who are full-time and part-time contractual employees are eligible for the SSP. A TRS employer must adopt the SSP for their employees to be eligible to participate. Retired and inactive TRS members are not eligible for the SSP.

How can I find out more about the SSP and register?

Interested TRS members who are eligible to participate are encouraged to visit the TRS SSP participant website at trsilssp.voya.com.

Your SSP Account

Participating TRS members can access their accounts online through the TRS SSP participant website at trsilssp.voya.com or via the toll-free TRS SSP Service Center at 844-877-4572 (844-TRS-457B).

Why Bring More with the SSP?

Reason 1: Your pension may not cover your entire retirement lifestyle, so supplementing your pension income is up to you through personal savings or an optional retirement savings plan like the SSP.

Reason 2: The longer you save, the more you will save and the more time your savings will have the potential to grow.

Reason 3: You have two types of contributions available and can pick the one that’s best for you. If you choose to contribute pre-tax, your account grows tax deferred and you pay taxes when you withdraw your money. If you contribute after-tax, your investments grow tax deferred and you enjoy tax-free income in retirement.

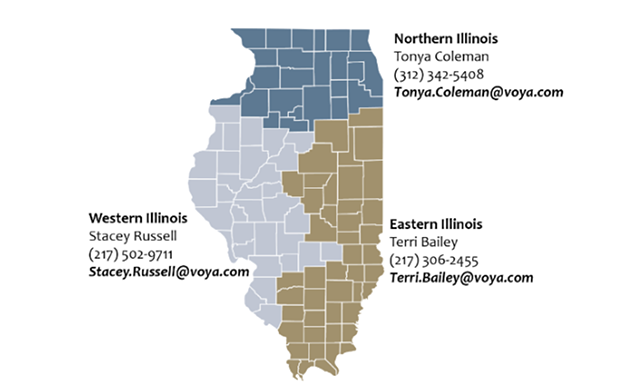

Connect with a Local TRS SSP Representative

Bring More to your retirement plans with the SSP. TRS and Voya have three representatives to specifically help eligible members learn more about the SSP. Note that a representative cannot give investment advice or monitor member accounts.

Your local TRS SSP representative will provide ongoing support to help meet your needs, including:

- SSP information and enrollment assistance

- Consolidation of retirement accounts

To schedule a virtual appointment with a local representative, go to https://trsssp457b.timetap.com.

Prepare for Retirement by Using This Retirement Time Line Checklist

As Soon as Possible

As Soon as Possible

If you have not already submitted a “proof of birth” online in the Member Account Access area, it must be provided to TRS in order to process your retirement benefit.

Update your years of service. Obtain the cost of reinstating a TRS refund, record sick leave from former employers and report optional service.

Types of optional service include:

- substitute teaching,

- homebound or part-time service before July 1, 1990,

- out-of-system service,

- military service,

- board-approved leaves of absence,

- leaves of absence due to pregnancy or adoption prior to July 1983,

- involuntary layoffs, and

- recognized Illinois private school service (Must apply on or before June 30, 2023).

Update your Beneficiary Designation form to ensure that survivor benefits will be paid according to your wishes.

Provide us with your home email address in the secure Account Access area. Emails about legislation and other important events will also be sent periodically.

Inquire about upgrading your pre-July 1998 service to the 2.2 formula. Call us for the cost to upgrade (Tier 1 members only).

Consider consulting with a financial planner. TRS does not provide financial advice.

Determine if any reciprocal service you have accrued will be beneficial to use in retirement. Each retirement system has specific rules about reinstating refunded service.

4 to 5 Years Before Retirement

Attend a pre-retirement meeting. A schedule is available on the TRS website during the fall.

Request a benefit estimate online in the secure Member Account Access area or by calling us. We will need to know your estimated retirement date; the number of unused, uncompensated sick leave days at retirement; and current and estimated future salary rates, including TRS contributions. Also include any bonuses and extra-duty pay.

2 Years Before Retirement

Request an updated benefit estimate (online or by phone).

Attend a pre-retirement meeting.

Finish reporting all optional service; this task may take time and research.

Complete payment to reciprocal system for refunded service, if applicable.

6-12 Weeks Before Retirement

Complete the Personalized Retirement Interview by calling us or logging on to the Member Account Access area of our website. You’ll be asked a few questions that will complete information in the retirement packet for you. You will receive the packet within 15 working days. If you have reciprocal service, you also will need to call the other retirement system(s) to apply.

Be certain you have provided us with your home email address in the secure Member Account Access area online. You will receive important information about the status of your retirement via email.

Check on the status of any optional service or 2.2 balances still owed (Tier 1 members only).

During the retirement process, you will be asked how you wish to pay any remaining 2.2 balance. Payment can be made either through a lump sum, rollover, or pre-tax reduction from your monthly annuity check. If you have any optional service balances, they must be paid prior to retirement, with the exception of pregnancy or adoption leaves.

TRS Investments Continue to Be Strong in 2021

The TRS investment portfolio ended calendar year 2021 in a very strong position despite growing uncertainty about the economy in the last half of the year.

At the end of December, the System’s investment assets totaled a record $66 billion. The 12-month investment return was 16.8 percent.

These results continue a consistent three-year upward movement in investment earnings. The System’s investment return was 13.4 percent at the end of calendar year 2019 and a 7.9 percent in 2020 while the world dealt with the COVID-19 pandemic.

Long-term, TRS investments continue to outperform the System’s long-term assumed rate of return of 7 percent. The 40-year rate was a 9.5 percent. The TRS investment strategy emphasizes steady, long-term growth in assets. The majority of members maintain a relationship with the System that lasts for 40 or 50 years – from the beginning of their careers in education to retirement for the rest of their lives.

Late in 2021, the TRS Board of Trustees notified the General Assembly and Gov. JB Pritzker’s office that under state law the state government contribution to TRS in fiscal year 2023 should be at least $5.89 billion.

The TRS Board is required at the end of each year to calculate and certify the state’s annual contribution to the System for the next fiscal year. The certified contribution is then forwarded to state officials for inclusion in the budget for the next state fiscal year. Fiscal year 2023 begins on July 1.

The fiscal year 2023 certified contribution is a 4 percent increase over the state’s $5.69 billion contribution for the current fiscal year.

Led by a strong 25.5 percent net investment return in fiscal year 2021 and a stable funding commitment from state government for the last few years, the System’s funded ratio inched up for the first time in several years – a sign of improving fiscal health. During fiscal year 2021, the ratio grew to 42.5 percent from 40.5 percent.

Still, TRS continues to have one of the lowest funded ratios in the nation among large retirement systems. And while the funded ratio is important as an official measure of the System’s long-term fiscal health, it is not a reflection of the System’s current financial ability to pay benefits.

In any given year, TRS only is obligated under state law to pay out the amount of money owed annually to retired members and other beneficiaries. During fiscal year 2021, benefits owed totaled $7.4 billion. TRS was more than able to pay all benefits for the year on time and in full. In fact, for 82 years TRS has paid all benefits in full and on time.

Members Should Be Alert for Potential Scams

TRS is encouraging members and annuitants to remain alert for potential scams that target your retirement system membership and benefits. We are hearing from members who have been solicited for retirement planning assistance claiming to know about your TRS benefits. These non-authorized individuals may give the impression they are affiliated with TRS when they are not.

TRS is encouraging members and annuitants to remain alert for potential scams that target your retirement system membership and benefits. We are hearing from members who have been solicited for retirement planning assistance claiming to know about your TRS benefits. These non-authorized individuals may give the impression they are affiliated with TRS when they are not.

Only TRS staff are authorized to provide information about TRS benefits and assist with your TRS retirement planning. TRS does not endorse or authorize anyone else to answer your TRS retirement questions or help you apply for TRS benefits.

The System is always watching for cybercriminal activity and scams that affect members and retirees. You can do your part by verifying the identify of anyone who sends you unsolicited mail, telephone calls or emails that suggest they have some connection to TRS.

As you remain vigilant against scams, here are a few things to remember:

- TRS will never call or contact you to endorse any company’s product or service relating to your TRS pension.

- Always carefully guard your Social Security number, birthdate, TRS account number, personal address and any other personally identifying information. Don’t share.

- Be wary of all links and attachments in unsolicited emails.

- Don’t be rushed into making any decision.

- Independently verify the identity of the person or company contacting you.

TRS is monitoring the internet and other forms of communication to spot trends and potential unauthorized activity directed at our members. TRS will take appropriate action when we become aware of individuals or businesses using misleading tactics to give a false impression that they are affiliated with TRS.

Members may help by contacting Member Services with tips about activities they find suspicious. If you hear from anyone that offers to enhance or better manage your benefit, always contact TRS before speaking or meeting with anyone who claims to have information about your TRS benefits.

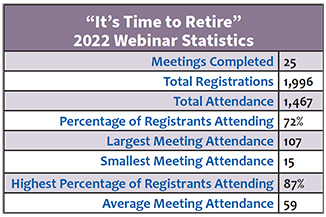

"It's Time to Retire" Webinars Held Successfully in Early 2022

For the second year, the TRS Member Services Department scheduled “It’s Time to Retire” webinars during January, February and March via WebEx for any members thinking about retirement during 2022.

The 25 meetings were designed to explain how to initiate the retirement process. Counselors reviewed the retirement paperwork and provided members with valuable information about TRIP health insurance and the limits on post-retirement employment.

If you are planning to retire in 2022, we encourage you to watch the "It's Time to Retire" meeting.

Response to this latest round of TRS webinars was well received, indicating that retiring members are eager for information about the retirement process.

Response to this latest round of TRS webinars was well received, indicating that retiring members are eager for information about the retirement process.

For those who retire this spring, “What’s Next?” webinar sessions will be offered this summer for new retirees. TRS will send session details to eligible members via email. "What's Next?" will remind the recently retired about post-retirement matters including post-retirement limits, taxes and TRIP/TRAIL insurance enrollment/transition.

Following the summer webinar series, the Member Services Department will schedule its traditional Fall Member Meetings in September, October and November. These large group sessions, held via WebEx in 2020 and 2021, are designed to help all members better understand TRS, not just those who are close to retirement.

Spring 2022. Published by the Teachers' Retirement System of the State of Illinois.